Purchasing real estate is both exciting and complex, and the mortgage process is often the most intimidating part for buyers. Understanding how financing works — from pre-approval to closing — helps buyers make informed decisions, avoid surprises, and move through the transaction with confidence.

Here’s a step-by-step breakdown of how the mortgage process works in a typical residential purchase.

1. Financial Preparation: Know Your Numbers

Before speaking with a lender, buyers should assess their financial profile. Lenders focus on several core factors:

- Credit score and credit history

- Debt-to-income (DTI) ratio

- Income stability and employment history

- Available funds for down payment and closing costs

Buyers are entitled to a free credit report annually from each bureau, which is a smart starting point. Even small credit improvements can impact loan options and interest rates.

Why this matters: Strong financial preparation improves loan terms and reduces the risk of delays or denial later.

2. Mortgage Pre-Approval (Not the Same as Pre-Qualification)

Pre-approval is a critical step that should happen before house hunting.

- Pre-qualification is an informal estimate based on self-reported information.

- Pre-approval involves documentation review (income, assets, credit) and a conditional lender commitment.

A pre-approval letter:

- Confirms your price range

- Strengthens purchase offers

- Identifies potential issues early

Most sellers — and listing agents — expect a valid pre-approval with an offer.

3. Choosing the Right Mortgage Loan

Buyers have multiple loan options depending on financial profile, goals, and property type.

Common loan programs include:

- Conventional loans (often backed by Fannie Mae or Freddie Mac)

- FHA loans (insured by Federal Housing Administration)

- VA loans (for eligible veterans)

- USDA loans (for qualifying rural areas)

Key decisions include:

- Fixed vs. adjustable interest rates

- Down payment requirements

- Mortgage insurance obligations

4. Making an Offer and Loan Application

Once under contract, the buyer formally applies for the mortgage.

This includes:

- Completing a Uniform Residential Loan Application (URLA)

- Submitting pay stubs, W-2s, tax returns, bank statements, and ID

- Locking in an interest rate (if desired)

Federal law requires lenders to issue a Loan Estimate (LE) within three business days, outlining:

- Interest rate

- Monthly payment

- Closing costs

- Cash needed to close

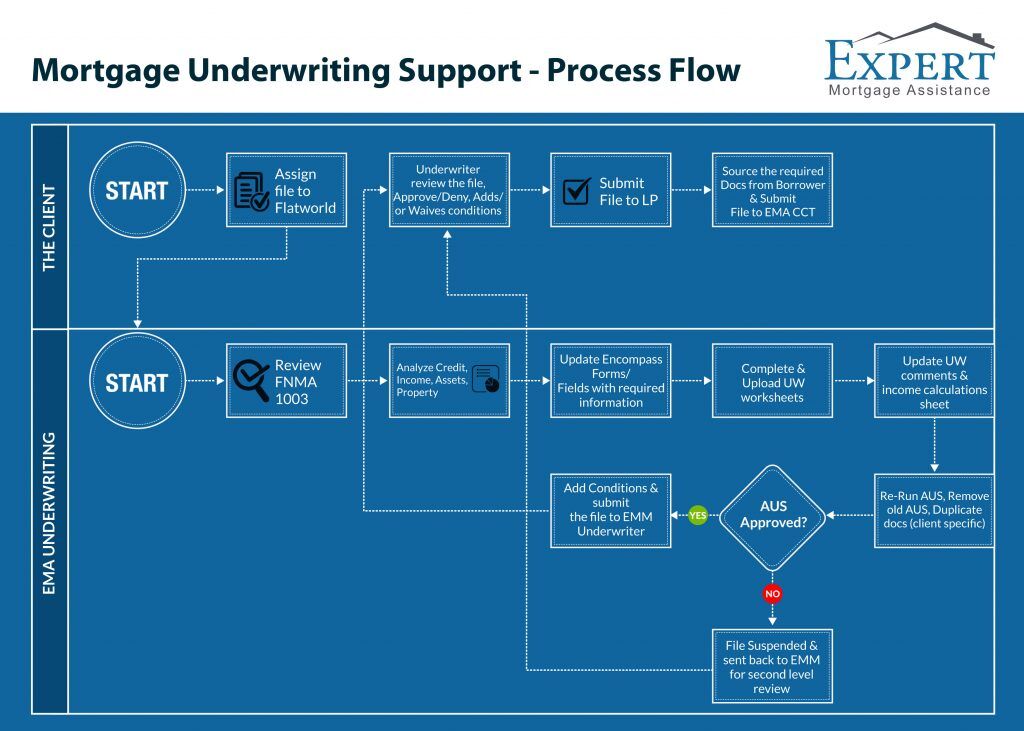

5. Underwriting: The Most Detailed Review

Underwriting is where the lender verifies all information and assesses risk.

The underwriter evaluates:

- Credit consistency

- Income and asset documentation

- Property appraisal

- Title work and insurance

- Contract terms

Buyers may receive conditions, which are additional documentation requests. Prompt responses are essential to keep the transaction on schedule.

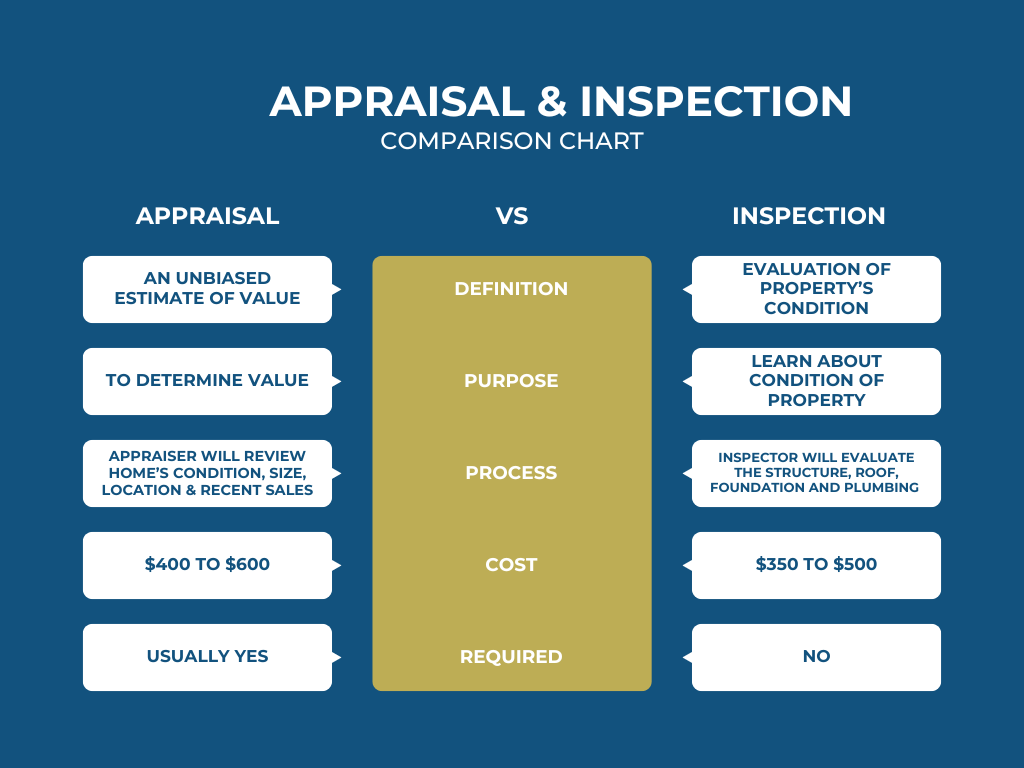

6. Appraisal and Property Review

The lender orders an appraisal to confirm the property’s value supports the loan amount.

If the appraisal:

- Meets or exceeds the purchase price → process continues

- Comes in low → renegotiation, additional cash, or loan adjustment may be required

This step protects both the lender and the buyer from overpaying.

7. Final Approval, Closing Disclosure, and Closing

Once underwriting is complete, the loan receives clear to close status.

Buyers receive a Closing Disclosure (CD) at least three business days before closing, which finalizes:

- Loan terms

- Interest rate

- Monthly payment

- Exact closing costs

At closing, buyers:

- Sign loan and title documents

- Provide remaining funds

- Receive keys once the transaction is recorded

Final Thoughts

The mortgage process isn’t just paperwork — it’s a structured financial review designed to ensure buyers can afford the home long-term. Buyers who understand each step are better positioned to choose the right loan, avoid stress, and close smoothly.

Working with an experienced real estate professional and a reputable lender ensures coordination, clear communication, and timely problem-solving throughout the transaction.